Would you like to download this whitepaper?

Operating as a Tax Group

July 17,2019 / Haroon Juma / VAT & Tax / Software Solutions

Cost & Risk Management of VAT Compliance and Reporting

The Benefits of Tax Grouping

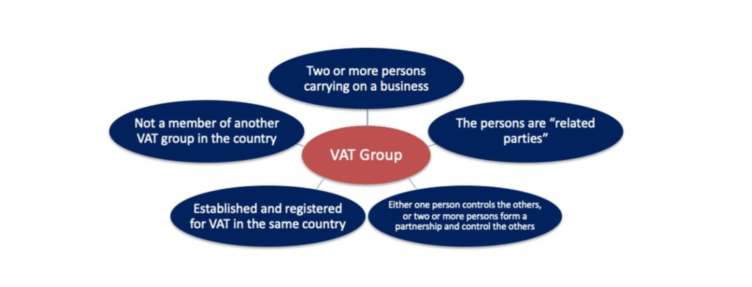

Under the UAE Executive Regulations, registering as a Tax Group can provide significant benefits to businesses reducing the complexities and compliance costs for VAT reporting.

Although the term ‘Group’ implies this provision applies to solely large companies, the UAE economy hosts many businesses that are connected as ‘related parties’ where either one person controls the othrs, or two or more persons form a partnership and control the others. Therefore, Grouping can serve companies of various sizes and recognizes there are many companies operating in the UAE economy that are ‘related parties’.

The key benefit of Grouping being supplies made between members of a VAT group are disregarded from VAT (i.e. no VAT is due on the supplies) and treated as Out of Scope for VAT. The companies registered as under the same VAT Group will file a Consolidated VAT return with the same reporting period and filing can share a single VAT reporting period and submission deadline. This is a major benefit if there are several parties where if ungrouped, they would be obliged to report and file VAT returns under Company registrations individually, manage and pay VAT for each company as per its filing deadlines and charge VAT on intra-group supplies, leading to an amplified impact on cashflow and management overheads.

In this paper, we share the challenges and approaches to improve operating as a Tax Group to minimize cost and risks.

Improving Your Approach

Operating as a Tax Group

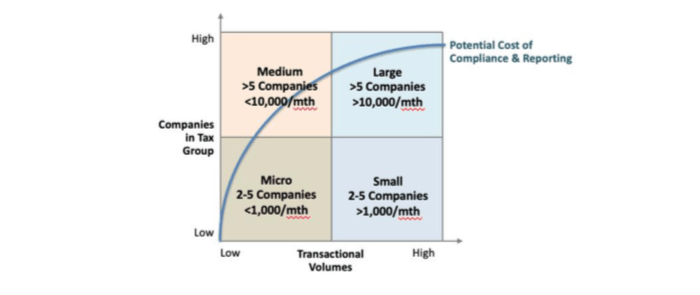

As a Tax Group, the scale and scope of your obligations and the potential cost of compliance will be dependent on the nature of your business (e.g. consumer/trade supplies, project services, importing/exporting) volume of transactions and the number of related companies in the Group.

As a general guide the higher the transaction volumes, the variety and related nature of transactions and the number of companies in the Group, the higher the complexities and cost of your Group compliance and reporting model.

Whatever your situation, the technology platform, centralized internal governance & processes and VAT expertise and policies become increasingly important as scope and scale increases to manage compliance, reporting obligations and risks.

Failing to assess, optimize and streamline these areas may create opportunity for errors, place pressure on your finance function to meet deadlines and lead to challenges to present transactional information in case of FTA audit. For Groups, these could lead to substantial administrative penalties based on the VAT amounts under question.

It is advisable and best practice to undertake a formal VAT assessment project and implement changes to improve your internal capabilities and implement a cost-effective model. In the UAE, there is evidence companies have paid limited attention to improving their cost of compliance and risk management. It would be wise to review and refresh your model especially as there is period of operation of the Tax Group to base against.

Impacts to Finance

Prior to the introduction of VAT, the role of central finance may have been limited to manage consolidation of financial reporting and report on internal performance of the individual companies.

This may have changed from January 2018 where they may have been tasked to control and report on VAT obligations. VAT places increased responsibilities on central teams to manage the implementation, controls, policies and reporting of VAT for the Group and adapt as the business or legislation evolves.

In addition, finance and business teams would also require support for any escalations. As a result, this forces the central team into the forefront for managing this on a timely basis. The larger the group, the greater the requirement for expert resources to guide and manage these obligations.

Improving Your Approach

For any central function, Governance and executive support are essential to empower central teams to roll out common policies and ensure they are supported by the individually companies. Whereas in the past the information flow may have been bottom up, this must change to a bidirectional flow to the businesses for your Group Tax structure to function correctly.

Impacts to IT

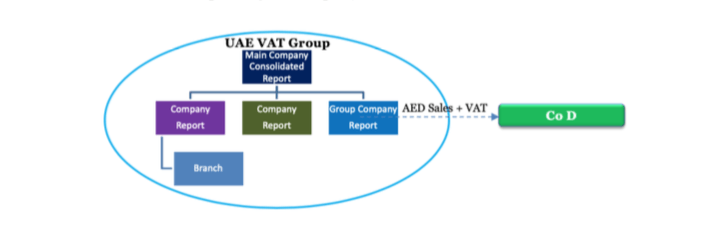

A critical component for Group Reporting is the IT application managing the transactional recording of supplies and purchases to enable a cost-effective way to manage /reporting costs and risks. Ideally your platform should:

-

Accurately record taxable supplies at Emirates level

-

Accurately recover purchase transactions and allow for blocked input VAT recovery

-

Record intercompany transactional flows as out of scope

-

Reporting capabilities to generate the tax reporting by transaction type

-

Create an audit trail with supporting document attachment from a filed VAT report to the specific transaction across the Group

It may be the case that your business operates different software platforms or does not support group reporting functionality that can provide a consolidated VAT report at the main level with focused reporting at company level.

This is a common issue and creates risk for errors and misreporting. System constraints could create a scenario where accounts payables/receivables ledger data is extracted from company systems to create a manually consolidated VAT report. This is inherently flawed and presents risk such as:

- The manually prepared consolidated VAT report not reconciling with your source data.

- During a reporting cycle, corrections made manually in the consolidated VAT report may not be acceptable unless the adjustments are reflected in the source data as well backed up by correct issue of Invoices and Credit notes as required.

- As the data is required to be retained for 5 years in accordance with the VAT Law, the risk is compounded if there is no proper audit trail in the event of enquiries or FTA audit

- FTA may require companies to start filing FTA Audit File (FAF) in the near future for which companies need to have proper accounting records and systems in place to report transactional files as required for VAT reporting.

Improving Your Approach

If you are seeking to improving this situation, a system-based model may require upgrading your existing IT systems or use other providers to support them with the required IT capability. Both options require careful planning, investment budgets, skilled resources and more importantly time. However, they will deliver benefits such to:

- Eliminate or reduce significantly any manual selection of tax codes to enable accurate recording and reporting of taxable supplies

- Enable use of selectable tax codes to correctly record Supplier invoices to enable accurate recovery of input VAT To improve accuracy of your recorded purchases and supplies to correct tax codes, the use of a transactional tax validation tool will significantly reduce the number of errors and misreporting issues caused by human or system errors.

Impacts to Internal Capabilities

A major contributor to a successful Group reporting model will be your company’s investment in human resources. Increasing the Group finance function’s skills and capabilities is essential and may also require injection of experienced resources. VAT can create unique challenges both on a commercial and financial basis and the Group function will be required to

- Input to contractual or commercial terms to manage cashflow impacts

- Lead the ongoing VAT reporting operational requirements

- Guide and advise operating finance teams on policies

- Act as escalation points

- Liaise with internal stakeholders to manage changes from new legislation

Research has shown a lack of attention on training and change management across the Group increases risks and can actually cost more than the required investment.

Summary

From our experience, these discussion points can improve the success of your Tax Group model. You may be faced with other challenges from a technical or business standpoint, however these factors represent the main areas of issues whether small or large business that can be better managed with:

- Enhanced visibility and sponsorship for central finance team

- Fit for purpose controls and governance

- Appropriate investment in IT

- Setting reliable and timely decision-making processes

- Filling capability gaps and resourcing appropriately

- On-going training and development to remain compliant In your assessment of your group reporting model, these pointers do not necessarily lead to major demands on your resources or investment. They may in reality reduce the financial impact to your business over the medium term and actually lead to better performance and cost of compliance.

Partner With SimplySolved

Serving over 200+ clients we know the challenges your business faces operating cost effective, compliant and efficient back office operations in Finance, Tax, Human Resources Management, IT and Marketing.

As an FTA Accredited Tax Agency with ISO 9001 Quality & 27001 Information Management Certification, we offer a quality-based approach to our services supported by dedicated team of certified professionals.

We support our clients with defined processes, platforms and expertise to deliver advisory, project and outsourced services in Accounting, Tax, Auditing, HRM, IT & Marketing. Our offerings are specially designed to meet the UAE Regulations to put you in control of your information, comply to the regulations and help you make better business decisions.